OHUB @ohub

🚨 OHUBNext | The Safety Net Is Being Financialized — And Households Are Carrying the Risk

🚨 OHUBNext | The Safety Net Is Being Financialized — And Households Are Carrying the Risk

Hey Builders,

The U.S. insurance system — the mechanism designed to protect families, retirees, businesses, and entire regions from catastrophic loss — is quietly being rewired.

Not by regulators.

Not by policymakers.

But by private equity.

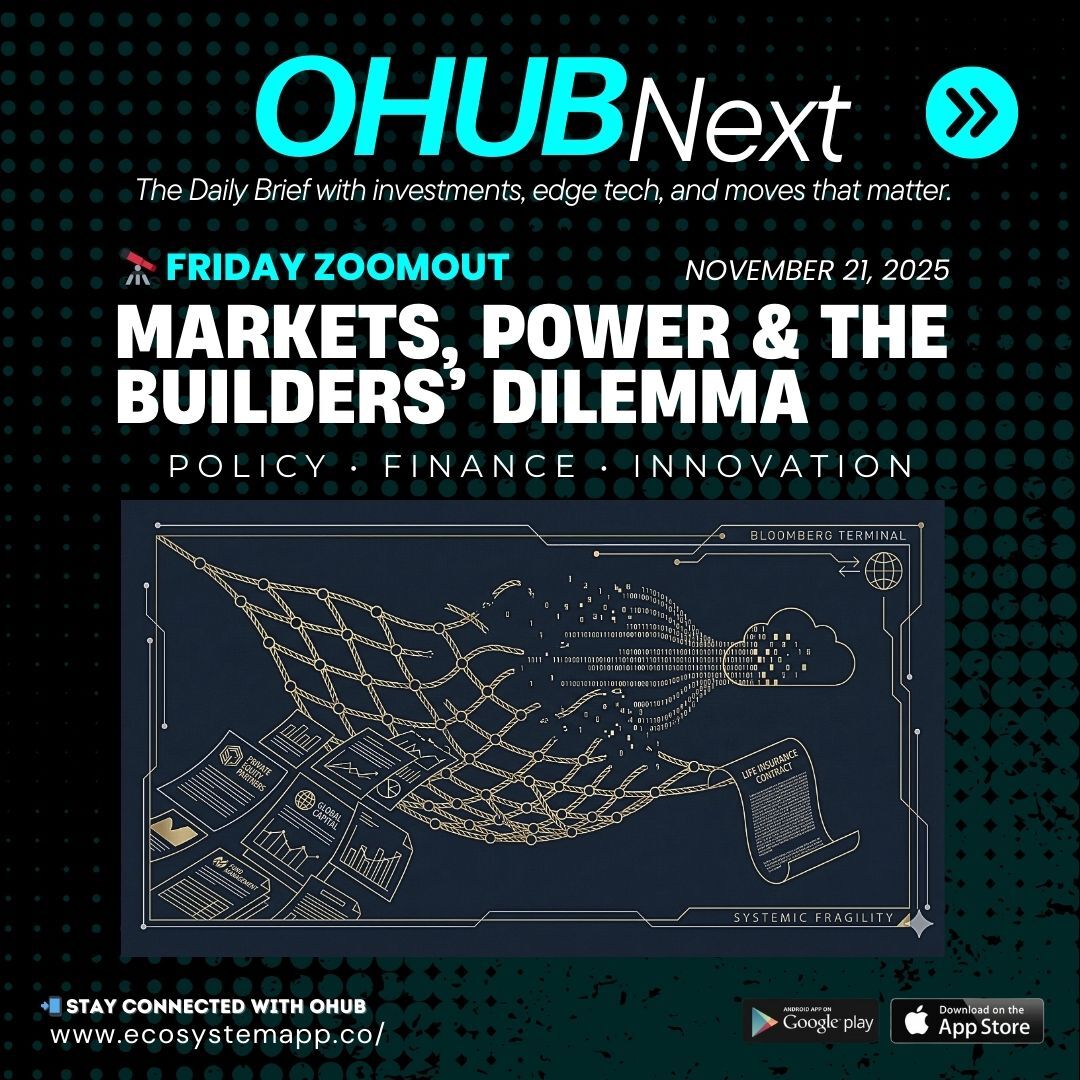

Over the last decade, a wave of P/E firms has acquired or taken controlling stakes in more than 100+ U.S. insurance companies, representing trillions in household assets (NAIC, A.M. Best). These deals are reshaping how risk is priced, how premiums rise, how claims are paid, and ultimately how financially vulnerable households become in moments when protection matters most.

This isn’t a headline story.

It’s a structural one.

And it has consequences for anyone trying to build generational wealth.

Today’s Friday ZoomOut breaks down what’s happening, why it matters, and what it means for your future planning.

⸻

🗞️ Top Story — The Private Equity Takeover of America’s Safety Nets

For most of the 20th century, insurance companies were conservative institutions: slow-moving, heavily regulated, and designed to prioritize solvency over returns.

That era is over.

Private equity firms — Apollo, Blackstone, KKR, Carlyle, Brookfield — have become some of the largest owners of U.S. life insurance and annuity companies.

Their strategy is simple:

1️⃣ Acquire an insurer

2️⃣ Move billions of policyholder assets into higher-yield, higher-risk investment vehicles

3️⃣ Capture the spread

4️⃣ Exit with profit — while households carry the long-term risk

This model isn’t inherently bad.

But in a sector designed to deliver guarantees, not yield, it creates a quiet shift:

Risk moves away from institutions and toward the families paying premiums.

⁉️ Why P/E Wants Insurance in the First Place

Because insurers have something private equity loves:

🪙 Long-term capital they can invest with discretion.

Life insurance premiums.

Annuity assets.

Pension rollovers.

Retirement accounts.

All of it becomes fuel for increasingly complex financial strategies — including credit instruments, structured products, and private credit portfolios.

And because regulators focus primarily on solvency, not investment transparency, consumers rarely see how their future promises are being restructured behind the scenes.

⸻

The Reinsurance Shuffle

Here’s the other part most people miss:

A massive share of U.S. insurance risk is being ceded offshore — mainly to Bermuda — where capital rules are far looser.

Bermuda reinsurers now play a critical role in the private-equity insurance pipeline:

▪️U.S. insurer sells policies

▪️Risk is offloaded to Bermuda reinsurer

▪️Assets are invested in higher-risk portfolios

▪️Consumers still expect guaranteed payouts

This allows firms to show strong balance sheets while taking more aggressive investment positions.

But “less regulation + more risk” is not a formula that ends well in a systemic downturn.

⸻

⚡ Quick Briefs

▪️ Private equity–owned insurers now manage more than $1.2 trillion in annuity and life assets (NAIC).

▪️ A top U.S. life insurer is now majority-owned by Apollo — and shifted more than ⅓ of its portfolio into alternative credit products (A.M. Best).

▪️ Florida, California, and Louisiana homeowners face historic premium spikes as reinsurers exit climate-exposed markets (Wharton Risk Center).

▪️ U.S. regulators warn that reinsurance transfers “obscure the true location of risk” across the financial system (GAO).

▪️ Consumer groups raise concerns about delayed payouts and reduced coverage flexibility in P/E-owned carriers.

⸻

🧱 Builder Insights — What This Means for Your Planning

1️⃣ If your insurer is owned by private equity, ask how your assets are invested.

Solvency might be fine — but volatility risk rises.

2️⃣ Diversify your safety nets.

Relying on one life policy, one P&C insurer, or one retirement vehicle is increasingly risky.

3️⃣ Understand the reinsurance chain.

If risk is being offloaded to lightly regulated jurisdictions, your “guarantee” is only as strong as the weakest link.

4️⃣ Climate and AI are now insurance events.

Both will reshape premiums, availability, and underwriting in the next three years.

5️⃣ Wealth is what you keep — not just what you earn.

Protection planning is becoming as important as investing.

⸻

💬 Quote of the Day

“Safety nets fail the moment they become profit centers.”

— Adapted from former FSOC advisors

⸻

🎬 Closing Thought — The Future of Risk Belongs to Those Who Understand It

The insurance system was built for stability.

It is now being redesigned for yield.

That doesn’t automatically mean collapse.

But it does mean households must become more sophisticated about their own risk exposure.

So here’s your challenge:

Audit your safety nets.

Understand who owns them.

Understand where your risk actually sits.

And understand whether the guarantees you’re relying on are still as solid as you think.

Because the next decade won’t just reward those who build wealth. It will reward those who protect it.

⸻

⚡ OHUBNext Daily Brief — investments, edge tech, and moves that matter.

For 12+ years, OHUB has been building pathways to multigenerational wealth through exposure, skills, entrepreneurship, capital markets, and inclusive ecosystems.